Overview

Although EBITDA is not recognized under Generally Accepted Accounting Principles (GAAP), its simplicity makes it a popular metric for comparing companies. However, critics argue it can overstate profitability, which is why the U.S. Securities and Exchange Commission (SEC) requires companies to reconcile EBITDA with net Income.

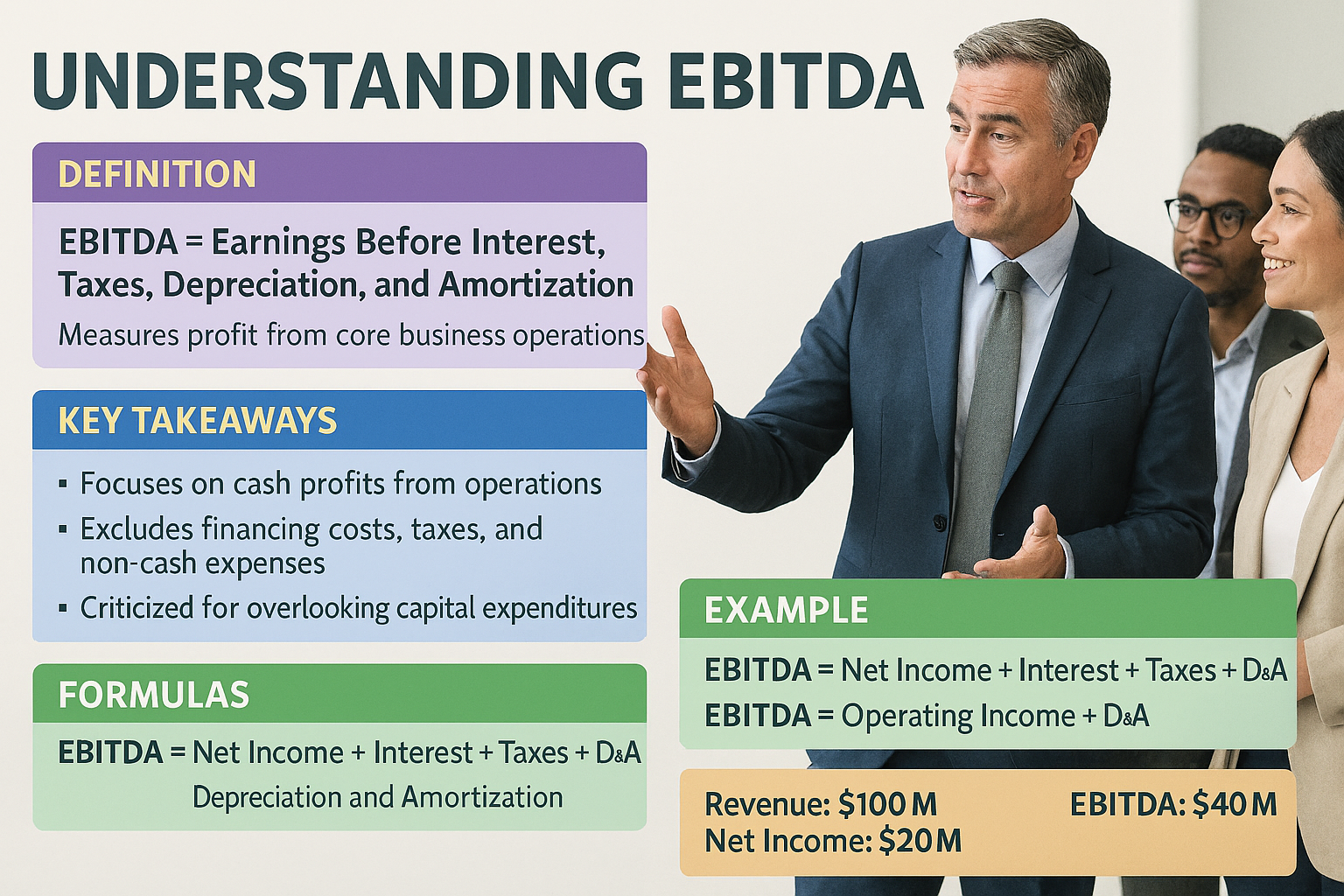

Key Takeaways

- EBITDA highlights a company’s operating profitability, helping investors assess fundamental health.

- It is calculated by adding interest, taxes, depreciation, and Amortization back to net Income.

- Critics, including Warren Buffett, argue that EBITDA ignores real costs like depreciation and capital expenditures.

- The SEC mandates reconciliation of EBITDA with net Income and prohibits reporting EBITDA per share.

EBITDA Formulas and Calculation

If a company doesn’t report EBITDA, you can calculate it from financial statements. Tools like Excel make this process simple.

- Net Income, tax, and interest appear on the income statement.

- Depreciation and Amortization (D&A) are usually found in the notes to operating Profit or on the cash flow statement.

Two common formulas:

· EBITDA = Net Income + Taxes + Interest Expense + D&A

· EBITDA = Operating Income + D&A

Both yield similar results because operating Income excludes non-operating expenses like taxes and interest.

What Does EBITDA Tell You?

By adding back interest, taxes, and non-cash charges, EBITDA focuses on cash profits from operations, making it useful for:

- Comparing companies with different financing structures.

- Valuation ratios like EV/EBITDA (Enterprise Value / EBITDA).

- Analyzing asset-heavy industries (e.g., energy, manufacturing) where depreciation can distort net Income.

- Early-stage tech or R&D firms that amortize intellectual property costs.

However, EBITDA has limitations. It ignores capital expenditures and depreciation—real costs that affect long-term sustainability. Warren Buffett famously said, “References to EBITDA make us shudder,” emphasizing the importance of understanding its limitations to avoid overconfidence in performance assessments.

Example

Consider a company with:

- Revenue: $100 million

- COGS: $40 million

- Overhead: $20 million

- Depreciation & Amortization: $10 million

- Operating Profit: $30 million

- Interest Expense: $5 million

- Pretax Income: $25 million

- Taxes (20%): $5 million

- Net Income: $20 million

EBITDA = Net Income + Taxes + Interest + D&A

= $20M + $5M + $5M + $10M = $40 million

Final Thoughts

EBITDA is a valuable tool for evaluating a company’s operational performance, especially when comparing businesses across industries or capital structures. However, it should never be viewed in isolation. Because it excludes critical costs such as depreciation and capital expenditures, relying solely on EBITDA can create an overly optimistic picture of profitability. For a balanced analysis, pair EBITDA with other metrics such as net Income, cash flow, and return on invested capital. In short, EBITDA is a starting point—not the whole story.