Summary:

California’s Assembly Bill 507 (Haney), signed into Law in October 2025, is a cornerstone of the state’s housing strategy to convert underutilized commercial buildings into housing. The bill establishes adaptive reuse as a “use by right” statewide, streamlines permitting through ministerial approvals, and authorizes local incentive programs to subsidize affordability. It aims to tackle two significant challenges: high vacancy rates in office/retail spaces and severe housing shortages, particularly in urban areas.

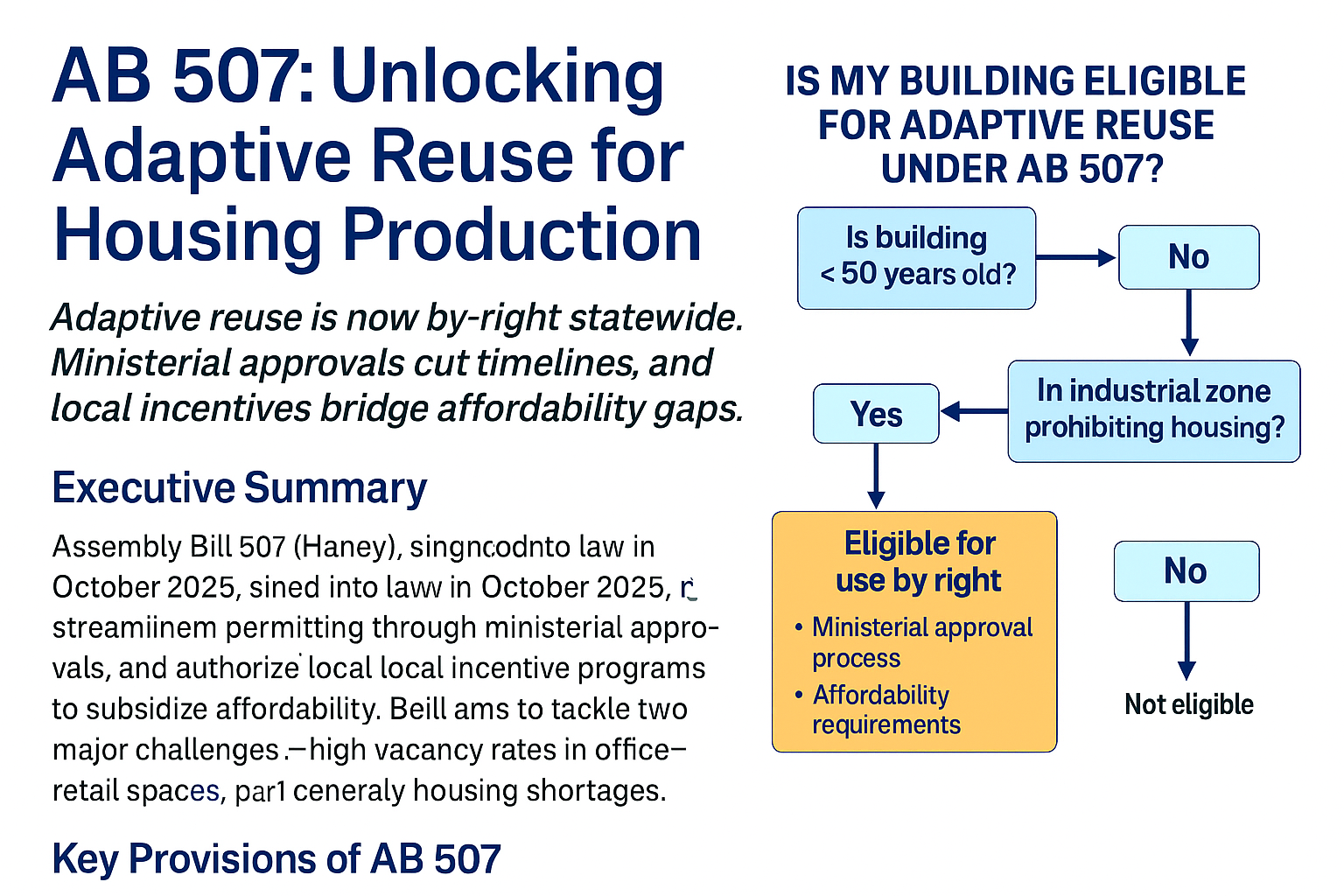

Key Provisions of AB 507

1. Adaptive Reuse as Use by Right

- Applies to existing buildings (generally less than 50 years old) or those meeting historic preservation standards.

- Overrides local zoning: Adaptive reuse projects are permitted in all zones except industrial zones, which prohibit residential uses.

- Requires compliance with the Secretary of the Interior’s Standards for Rehabilitation for historic structures or eligibility for state/federal historic tax credits. ,

2. Streamlined Ministerial Approval

- Adaptive reuse projects that meet statutory criteria qualify for ministerial review, eliminating the need for conditional use permits and discretionary hearings.

- Parking requirements are waived for portions of buildings that do not have existing on-site parking.

- CEQA review is effectively bypassed for qualifying projects under this ministerial framework.

3. Affordability Requirements

- Rental housing:

- Option A: 8% very low-income + 5% extremely low-income units

- Option B: 15% lower-income units

- Owner-occupied housing:

- Option A: 30% moderate-income units

- Option B: 15% lower-income units

- Mixed-use projects: At least 50% of square footage dedicated to residential use.

4. Local Incentive Programs

- Cities/counties may create Adaptive Reuse Investment Incentive Funds starting FY 2026–27.

- Funding source: incremental property tax revenue from increased assessed value post-conversion.

- Duration: Up to 30 years of payments to subsidize affordable units.

- Flexible structure: Funds can flow to owners or lessees under approved agreements.

Why AB 507 Matters

- Addresses office vacancy crisis: California’s urban centers face record-high commercial vacancies post-pandemic.

- Accelerates housing production: Ministerial approvals cut years off timelines.

- Supports affordability: Mandatory income-restricted units + local tax-increment incentives.

- Climate-smart development: Reusing existing structures reduces embodied carbon and infrastructure strain.

Implementation Roadmap

For Developers

- Eligibility check: Building age (<50 years) or historic compliance affidavit.

- Affordability strategy: Choose a rental or ownership compliance path early.

- Documentation: Prepare ministerial application with objective standards; no CEQA EIR required.

- Financing: Explore local incentive programs + state/federal historic tax credits.

For Local Governments

- Adopt ordinances for incentive programs by FY 2026–27.

- Set clear timelines for ministerial review (align with SB 35 shot clocks).

- Publish guidance on affordability verification and incentive fund requests.

Risks and Challenges

- Infrastructure capacity: Older buildings may need seismic, ADA, and utility upgrades.

- Historic compliance costs: Meeting preservation standards can raise project budgets.

- Local fiscal Impact: Diverting property tax increments for incentives may strain budgets.

- Market uncertainty: Conversion economics depend on construction costs and demand for smaller units.

Legislative Journey

- Introduced: 10 February 2025

- Passed Assembly: 23 May 2025 (64–1)

- Passed Senate: 10 September 2025 (30–9)

- Signed by Governor: 10 October 2025

- Effective Date: 1 January 2026

Key Takeaways

- Adaptive reuse is now by-right statewide (with exceptions).

- Ministerial approvals + CEQA bypass = faster conversions.

- Affordability mandates ensure equity.

- Local tax-increment incentives can bridge financing gaps.