Summary:

AB 480 (Quirk‑Silva) modernizes California’s Low‑Income Housing Tax Credit by unlocking flexible, later-stage credit sale elections and aligning administrative rules across the Personal Income Tax, Corporation Tax, and Insurance Tax codes. The bill allows sponsors to elect, at any time before final allocation, to sell all or a portion of state LIHTCs to unrelated parties, replacing the prior “elect‑at‑application” constraint that often resulted in depressed pricing and delayed closings. The measure was enrolled on 11 September 2025, passed both chambers with unanimous votes, and is included in the Governor’s housing package of O10 October It takes effect on 1 January 2026, and applies to projects with preliminary reservations made on or after J1 January 2016 ,

At a time when construction and interest costs are elevated, AB 480’s election flexibility can raise net credit pricing, shorten capital stacks, and reduce gap‑funding needs, including for farmworker housing—all while keeping California’s four-year state credit, 30-year affordability, and CTCAC oversight intact. This means that the bill has the potential to make housing more affordable for low-income individuals and families.

Background: How California’s LIHTC works (and why flexibility matters)

California administers the state LIHTC in modified conformity with federal §42: the state credit is claimed over four years (vs 10 years federally), requires 30-year affordability (vs 15 years federally), and is allocated by the California Tax Credit Allocation Committee (CTCAC) in tandem with federal awards or federal eligibility. Historically, a developer had to decide at application whether to “sell” state credits to an outside taxpayer; missing that box locked the sponsor out, reducing options later when market pricing, rates, or construction budgets changed.

The legislative counsel digest for AB 480 amends Revenue & Taxation Code §§ 12206 (Insurance), 17058 (PIT), and 23610.5 (Corp.), the core state LIHTC sections. It reaffirms CTCAC’s authority and the program’s scope (including farmworker housing) while focusing the statutory change on when and how the credit‑sale election is made.

What AB 480 changes (and what it doesn’t)

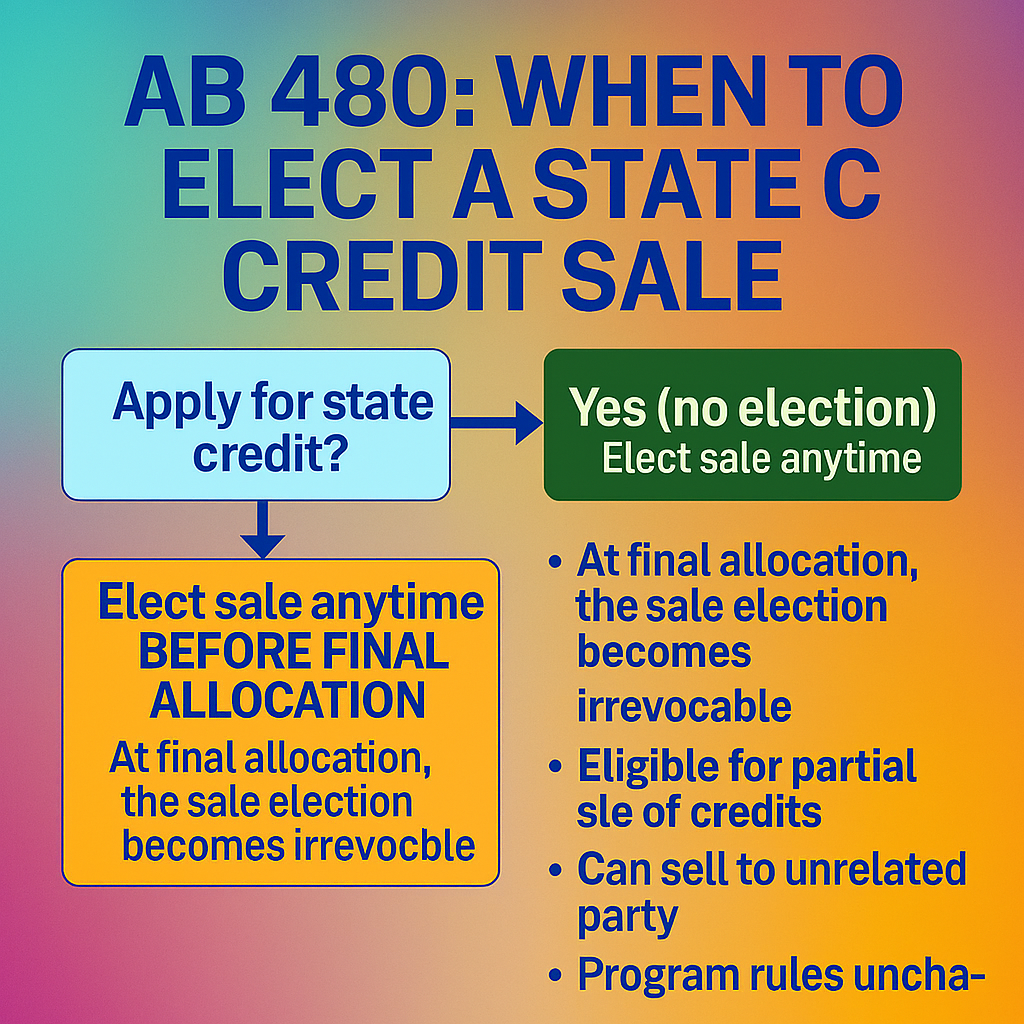

1) Election timing—moved from “at application” to “any time before final allocation.”

Sponsors may elect, in a manner prescribed by CTCAC, to sell all or any portion of the allowable state credit before CTCAC allocates the final credit amount; at that moment, the election becomes irrevocable. This eliminates the prior rule that forced an election on the application (and barred later changes).

2) Sale mechanics—apparent authority to sell to one or more unrelated parties.

The statute expressly authorizes a sale of all or part of the credit to one or more unrelated taxpayers, giving sponsors the ability to syndicate state credits in the format and timing that clears capital gaps most efficiently. (CTCAC will implement the mechanics via guidance.)

3) Consistency across tax codes; program fundamentals unchanged.

AB 480 amends the Insurance, PIT, and Corporation tax credit provisions together, so sale authority and election timing are uniform for insurers, C-corporations, S-corporations, partnerships, and individuals. It does not change the state credit’s four-year claim, 30-year affordability, or CTCAC allocation regime anchored in federal ≤§42 conformity.

Policy intent in one line: More flexible timing → better pricing and more buyers → larger private equity checks → fewer public subsidies per unit. Housing practitioners and advocates (e.g., CHPC, MidPen) supported AB 480 for precisely this reason.

“Allocated” vs. “Certificated” credits—why investors pay differently

California’s state LIHTC comes in two delivery models commonly described by practitioners:

- Allocated state credits behave like a flow-through benefit in the project’s ownership structure; investors typically need an ownership stake to claim them, and the state‑tax reduction can interact with federal tax deductibility of state taxes.

- Certificated credits are stand‑alone certificates that an unrelated taxpayer can purchase without taking a Partnership's's interest—functionally closer to a tax payment instrument for California liability. Because certificated credits avoid specific federal tax side effects, buyers often pay higher prices per state-credit dollar. AB 480 removes timing rigidities, allowing sponsors to choose the optimal path when market bids are real, not hypothetical.

The CHPC fact sheet explains why locking the election at application left money on the table: developers could not pivot to certificated credits after the award to capture superior pricing once actual term sheets materialized. AB 480 authorizes this pivot before final allocation, subject to the CTCAC process.

Legislative timeline and status

- Introduced: 10 February 2025 (Quirk‑Silva)

- Assembly passage: 2 June 2025 (79‑0)

- Senate passage: 4 September 2025 (39‑0)

- Enrolled/presented to Governor: 11 September 2025

- Included in the Governor’s 10 October 2025 housing package (signing day for multiple streamlining bills)

- Effective date: 1 January 2026; operative for projects with preliminary reservations on/after 1 January 2016.

Expected impacts on capital stacks

A) Higher net equity from state credits

Later-stage election windows allow sponsors to court more buyers (insurers, banks, and large corporates with California liability) and time the sale to coincide with construction milestones and market rates—typically increasing the price per state credit dollar and reducing the gap that must be filled with scarce soft funds. Practitioners anticipate stronger bids for certificated structures when buyers can purchase credits without ownership and without federal tax drag.

B) Faster closings and fewer re-underwrites

When markets move (such as Treasury yields, construction costs, and rent comps), sponsors previously had to reopen public gap requests or resequence applications. With AB 480, sponsors can respond by switching to a sale election before final allocation, thereby reducing the frequency—and political cost—of post-award subsidy requests. The Franchise Tax Board analysis explicitly frames the bill’s purpose as making it easier to elect sale of credits, with CTCAC prescribing the process.

C) Broader applicability, including farmworker housing

Because the LIHTC statutes (as amended) continue to encompass farmworker housing within the program scope, improved pricing should marginally increase the feasibility of projects in agricultural regions where deep rents and infrastructure costs are challenging.

Implementation roadmap

For developers/sponsors

1. Underwrite dual paths (allocated vs certificated): price each with current market indications; update at 90–120 days before estimated final allocation to decide.

2. Document election per CTCAC guidance: expect standardized forms, sale agreements, and timing checkpoints tied to final allocation.

3. Coordinate with federal LIHTC investor: ensure Partnership's's docs recognize potential state‑credit sale to an unrelated buyer and address guaranties/indemnities accordingly.

4. Sequence with soft loans: notify public lenders (HCD, locals) when state credit proceeds rise; adjust gap‑funding asks.

For investors (buyers of state credits)

- Establish purchasing platforms for certificated and allocated structures; track tax‑liability calendars and credit carryforward rules; price risk around delivery timing (tied to placed‑in‑service and CTCAC final allocation).

- Compliance posture: although the buyer claims the credit, the seller remains responsible for credit obligations under program rules; expect CTCAC/FTB to require information exchange and timely reporting.

For CTCAC & FTB

- Issue procedural guidance: form of election, deadlines keyed to final allocation, and attestations for unrelated‑party sales; maintain controls against double sale or mismatch with federal awards.

- Data transparency: Publish pricing bands by structure (allocated vs. certificated) to inform policymaking and monitor whether AB 480 lifts equity and reduces subsidy per unit as intended.

Risks and guardrails

- Market volatility: If investor demand cools or corporate tax liabilities shrink, later election flexibility helps—but does not eliminate—pricing risk. Sponsors should maintain backup election paths until the final allocation is made.

- Compliance exposure: The seller typically remains on the hook for program compliance (habitability, rent/income tests, recapture triggers). Contracts must clearly allocate recapture risk and indemnities to ensure transparency and accountability.

- Administrative integrity: CTCAC must enforce the timing and unique identification of credits to prevent double-selling or off-cycle transfers; election irrevocability at final allocation is a key control.

How AB 480 interacts with other 2025 housing reforms

The Governor’s 2025 housing package combined permitting streamlining and CEQA modernization (budget trailer bills AB 130/SB 131) with targeted supply-side tools, such as AB 480. Faster approvals mean capital needs to be ready when projects clear entitlements; flexible credit-sale timing helps sponsors lock in equity at the right moment, rather than making a guess a year in advance. [www.coveredca.com], [www.santa-ana.org]

Metrics to watch (2026–2028)

- Average state‑credit price (¢/credit‑$) by structure, pre‑ and post‑AB 480.

- Gap‑funding per unit in 9% and 4%+state‑credit deals, urban and rural.

- Share of projects electing sale after award (pre-final allocation) vs at application.

- Time‑to‑close (credit award → financial close) and rate of post‑award re‑underwrites.

- Farmworker housing allocations utilizing sale elections.

Frequently asked questions

Q1: Does AB 480 increase the overall amount of state LIHTC?

A: No. It changes the timing of elections and sale mechanics, not the annual cap or award criteria. CTCAC still allocates within statutory limits and the existing set-asides. [www.hcd.ca.gov]

Q2: Can I split the state credit among multiple buyers?

A: Yes—AB 480 expressly authorizes the sale of all or any portion to one or more unrelated parties, as prescribed by CTCAC rules. [experience...arcgis.com]

Q3: When must I decide?

A: Any time before CTCAC’s final allocation to your project. At final allocation, the election becomes irrevocable. [experience...arcgis.com]

Q4: What about projects awarded years ago?

A: The bill is effective 1/1/2026 and operative for projects with preliminary reservations on/after 1/1/2016—a broad cohort that can benefit at the final allocation stage if still pending. [experience...arcgis.com]

Conclusion

AB 480 is a practical, high-leverage fix: it doesn’t add a dollar to the state cap, yet it can raise the value extracted from each state credit by allowing sponsors to elect the optimal sale structure when market conditions are known in a tight financing environment, that translates into larger private equity checks, smaller public gaps, and more doors delivered—including in the hardest‑to‑serve rural and farmworker communities. With clear CTCAC guidance and robust reporting, California can track the uplift and iterate quickly if further calibration is needed. [experience...arcgis.com], [ca-adu.com]

Sources

- Bill text & code sections (Rev. & Tax. Code §§ 12206, 17058, 23610.5): AB 480 bill text & digest; enrolled status. [www.hcd.ca.gov]

- Status & votes: FastDemocracy tracker (enrollment 9/11/2025; 79–0 and 39–0 votes). [www.cityof...oledad.com]

- Governor’s package (10 October 2025): Press release listing AB 480 among signed housing bills. [www.santa-ana.org]

- FTB bill analysis (program mechanics; election timing; operative date and cohort): Franchise Tax Board analyses (intro & final). [www.veeto.app], [experience...arcgis.com]

- Program context; certificated vs allocated; rationale for higher pricing: CHPC/Assembly fact sheet; MidPen support letter. [ca-adu.com], [www.lacons...liance.com]

- Broader 2025 reforms (CEQA/streamlining): Governor’s budget trailer release (AB 130/SB 131) and legal summaries. [www.coveredca.com]